Legal Reckoning for Bengaluru’s ₹40 Crore Chit Fund Scam: Applicable Laws and SACM Provisions in Focus

Legal reckoning for Bengaluru’s ₹40 crore chit fund scam read the law.

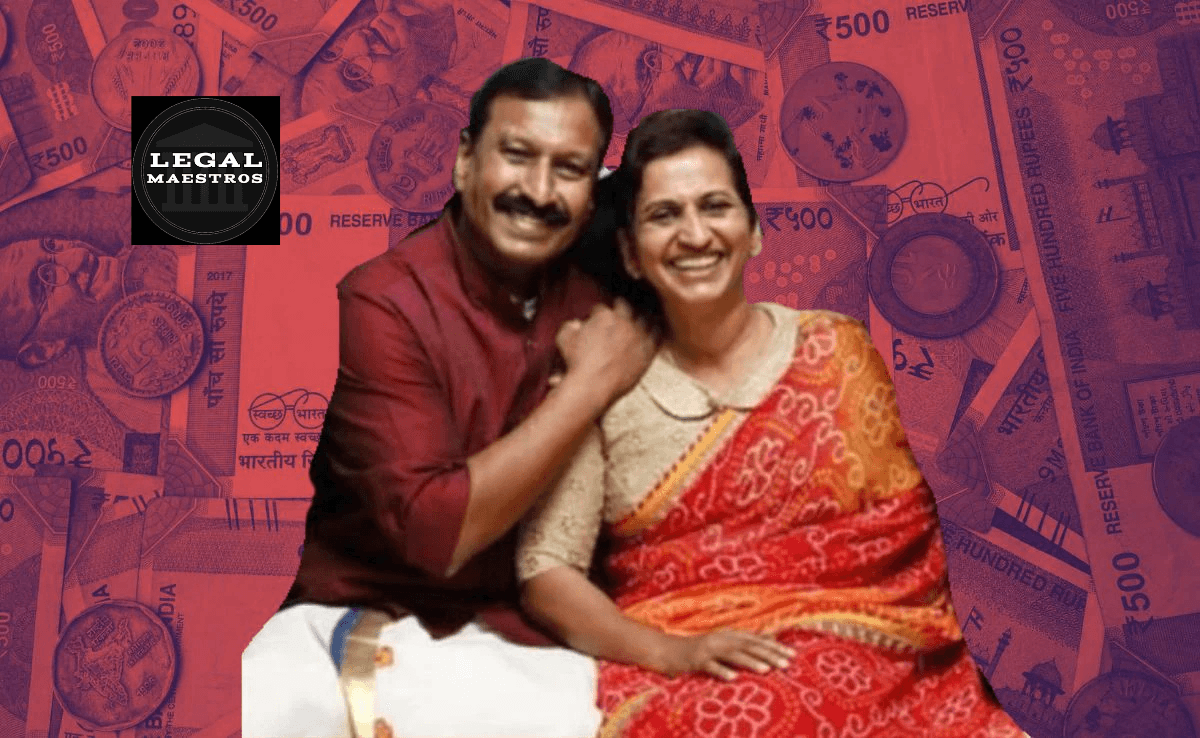

Bengaluru, a thriving city and a center of creativity, is a city where scams can flourish, taking advantage of the faith and dreams of innocent residents. The recent expose of a Rs 40 crore chit fund scam perpetrated allegedly by a Kerala couple has shaken investors. More than 260 souls have apparently lost their hard-earned cash, underscoring the necessity to know the legal statute concerning such schemes and the safeguards afforded to depositors.

Knowing chit funds and the cheat

Before we get into the law, let’s understand chit funds. Just picture a bunch of buddies or relatives who choose to save as a team. Each month, everyone puts the same amount into a pot. Then, an individual wins the whole combined pot. So this is a chit fund in a nutshell. In a more official chit fund, there’s generally a ‘foreman’ or a company managing the fund, who gets a small cut. Members can bid for the lump sum, usually at a discount, and share it with their fellow members. It’s a time-honored system that serves as both a savings and a borrowing account.

The Bengaluru scam is a case study in how to abuse this old system. The accused couple, Tommy A Varghese and Shiny Tommy, allegedly ran A & A Chit Funds and promised unusually high returns on fixed deposits, far exceeding what legitimate financial institutions could offer. This is the classic red flag in these scams: the promise of quick, outrageous returns that causes investors to overlook the obvious risk. Over time, as more investors were attracted by early payouts, the scheme expanded. As is typical with these fraudulent schemes, the payments ceased abruptly, leading to the disappearance of the husband and wife pair, leaving behind a group of investors who were devastated. That’s what’s called a ponzi scheme, where early investors get paid with money from new investors, rather than real profits, and the pyramid crashes in the end.

For any queries or to publish an article or post or advertisement on our platform, do call at +91 6377460764 or email us at contact@legalmaestros.com.

For More Updates & Regular Notes Join Our Whats App Group (https://chat.whatsapp.com/DkucckgAEJbCtXwXr2yIt0) and Telegram Group ( https://t.me/legalmaestroeducators ) contact@legalmaestros.com.

Protecting Depositors and Pursuing Fraudsters

So huge financial scams are dealt with in India under a robust and specialized set of laws designed to protect depositors, imprison perpetrators, and recover misappropriated assets.

The chit funds act, 1982

The nearest relevant existing statute is The Chit Funds Act, 1982. This is the main law providing a statutory framework for the regulation of chit funds in India. It aims to protect and bring transparency to subscribers (investors) in registered chit funds.

In accordance with The Chit Funds Act, 1982, every chit fund is to be registered with the Registrar of Chits. Unregistered chit funds are illegal. In the Bengaluru scam, if A & A Chit Funds was operating without proper registration, it would be a direct violation of this section.

Section 5 of the Chit Funds Act, 1982, prohibits carrying on any chit business without prior sanction from the state government. This once more brings to the fore the stringent regulatory control on chit fund business.

The Act sets out rules for the creation of chit agreements, the responsibilities of the foreman, and dispute resolution mechanisms. If the purported couple refused to abide by these steps, they would be in contravention of the Act.

Because the scam occurred in Bengaluru, the state-specific law, The Karnataka Protection of Interest of Depositors in Financial Establishments Act, 2004 (KPID Act), stands of great relevance. This Act was enacted to protect depositors in banks and authorizes the attachment and forfeiture of properties secured by fraud.

Section 3 of the KPID Act criminalizes any financial institution that fails to return deposits or defrauds depositors. This is the portion that counts for directly billing individuals in the scheme. Consider the depositor, an office boy, who banked his life savings in this scheme, to find the “institution” is gone. This Act provides such victims a remedy.

Section 4 of the KPID Act authorizes the government to attach properties of financial institutions alleged to have cheated. This is crucial protection for reclaiming the investors’ whirlpool losses. Imagine the police seizing the mansions, cars, and bank accounts of the accused and using them to compensate defrauded depositors.

Section 9 of the KPID Act defines punishment for offenses under it, with provisions for imprisonment and heavy fines. This ensures that the thieves who defraud depositors are imprisoned.

The KPID Act establishes Special Courts to try financial irregularity cases, offering speedy justice.

The PMLA or Prevention of Money Laundering Act, 2002

When the scam is big and attempting to wash the dirty source of those piles of cash, PMLA enters. Money laundering is making ill-gotten gains look legitimate.

- PMLA Section 3 defines money laundering crime as any person, directly or indirectly, attempting to indulge, or knowingly assisting or knowingly becoming a party to or actually involved in, any transaction or activity related to the crime proceeds and representing it as clean possession. If the couple instead squirreled the ₹40 crore through other bank accounts or into other assets to hide its fraudulent origin, then they would be liable under this section. Think of it like a thief ‘laundering’ stolen goods.

- Section 4 lays down the punishment for money laundering: rigorous imprisonment of three to seven years and a fine.

- The PMLA permits attachment and confiscation of properties derived from or involved in money laundering. That means authorities can confiscate any assets, in India or overseas, that were purchased with the swindled funds yet another way of potentially helping victims recover losses.

The BNS, 2023 (erstwhile IPC, 1860)

Sure, certain financial laws hold, and so do the underlying criminal laws. Bharatiya Nyaya Sanhita, or BNS, 2023, which superseded the Indian Penal Code, 1860, has provisions for cheating, criminal breach of trust, and criminal conspiracy.

- Section 318 of the BNS (Section 420 of the old IPC) is for ‘Cheating and dishonestly inducing delivery of property.’ That’s a typical allegation in financial corruption cases; the defendants usually con folks out of their money.

- ‘Criminal breach of trust’ falls under Section 316 of the BNS, not 406 or 409 of the old IPC. If the defendant was holding investors’ funds as a fiduciary and then converted them to their benefit fraudulently, this would be it.

- Section 61 BNS (and 120B of the old IPC) is ‘criminal conspiracy,’ where two or more people conspire to do an illegal act. Since this scam reportedly involved a pair, criminal conspiracy charges are almost a certainty.

What Asset and Configuration Management (SACM) Provisions Are Responsible For doing

In the context of Indian criminal law, the phrase “SACM provisions” does not refer to a specific legal term for financial scams; rather, it is essential to have a greater understanding of what it entails. The term “Service Asset & Configuration Management” (SACM) refers to a notion that is mostly associated with IT service management (ITSM) and focuses on the management of IT assets and the configurations of those assets across time. Making sure that the information on IT assets is accurate and up-to-date is made easier by this.

But for financial crimes, asset tracking and management is as important for investigation and recovery as for other goals. It is necessary for investigative agencies to employ “SACM-like” effective tactics, even if it is not a formal statutory requirement:

Keeping Accurate Records: In the same way as SACM maintains accurate configuration information, investigators need to maintain precise records of how money flows, transactions, and who owns what to construct a strong case and make it simpler to retrieve items where they belong.

Forensic accounting uses various specific methodologies to uncover hidden assets and track illegal activities. This is analogous to how SACM educates us about the interdependencies and connections between the various components of information technology.

1 thought on “Legal Reckoning for Bengaluru’s ₹40 Crore Chit Fund Scam: Applicable Laws and SACM Provisions in Focus”